미 연준 (FED)은 이번 6월 FOMC에서 역사적인 75 bps 정책금리 인상을 단행했다. 1994년 11월 이후 최초의 75 bps 인상.

아래는 이번 FOMC 전에 런투노가 적은 예상 글.

2022.06.13 - [기관투자노트/중앙은행 정책] - 2022.6.15 미 연준 FOMC 통화정책발표 전망: Why not hike 75 bps now?

2022.6.15 미 연준 FOMC 통화정책발표 전망: Why not hike 75 bps now?

지난주 미국 5월 소비자 물가지수 (US CPI) 발표 이후에 아래와 같이 적었다. 또한 오늘 지표로 인해 다음 주 FOMC에서 미 연준 (FED)이 75 bps 인상에 나설 가능성이 최소한 반반이라고 판단하고 있다.

londonin.tistory.com

정책발표 문구는 위의 예상에서 크게 벗어나는 내용은 없었지만, 함께 발표한 경제전망 (SEP)은 몇 가지 흥미로운 부분이 있었다. 또한 기자회견에서 연준 및 파월 (Powell) 의장의 속내를 짐작할 수 있는 몇 가지 단서도 보였다.

1. 정책발표

미 연준은 결국 지난주 나온 높은 소비자 물가지수 (CPI) 및 높아지는 기대 인플레이션을 감안, 75 bps 인상에 나섰다. 흥미로운 점은 현재 연준 구성원 중에서 가장 매파적인 사람 중 한 명이 50 bps 인상에 투표하는 소수 의견을 냈다는 점.

Voting against this action was Esther L. George, who preferred at this meeting to raise the target range for the federal funds rate by 0.5 percentage point to 1-1/4 percent to 1-1/2 percent.

https://www.federalreserve.gov/monetarypolicy/fomcpresconf20220615.htm

The Fed - June 14-15, 2022 FOMC Meeting

Please enable JavaScript if it is disabled in your browser or access the information through the links provided below. June 14-15, 2022 FOMC Meeting Accessible Keys for Video [Space Bar] toggles play/pause; [Right/Left Arrows] seeks the video forwards and

www.federalreserve.gov

그 외 QT나 administrative rate 등 다른 측면에서 크게 놀라운 내용은 없었다.

2. 경제전망 (SEP)

경제전망 수정에서는 의미 있는 변화가 많았다.

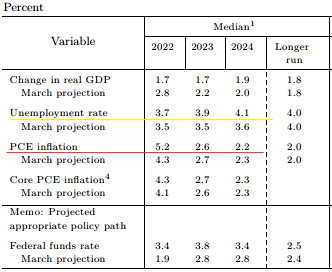

우선 물가 전망 (PCE, 빨간색)을 상당히 상향 조정한 것이 눈에 띈다. 동시에 실업률 (노란색) 또한 상향 조정했다. 이 수치대로라면 여전히 연준은 연착륙 (soft landing)의 가능성을 높게 보고 있음을 알 수 있다. 연준의 희망사항이 상당히 반영된, 런투노 생각에는 비현실적인 낙관적 전망이라고 생각한다.

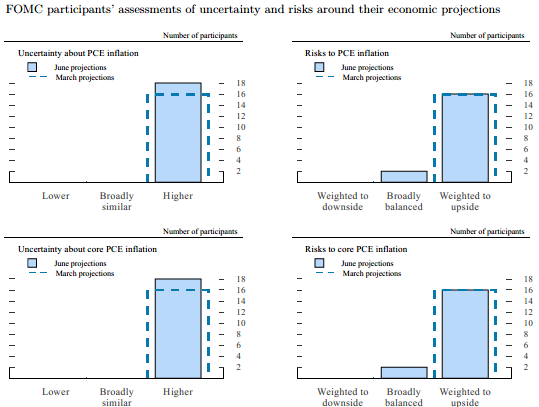

더 재미난 부분은 연준 FOMC 구성원들의 물가에 대한 전망. 지난 3월에는 한 명이 물가 전망에 대해 중립적인 입장을 취했다면, 이번 6월에는 FOMC 구성원 전체가 만장일치로 물가상승률에 대한 upside risk가 더 크다고 답변했다. 최근 통계에서 확인할 수 있는 물가 상승 압력에 대한 연준 FOMC 구성원들의 걱정을 읽을 수 있는 대목.

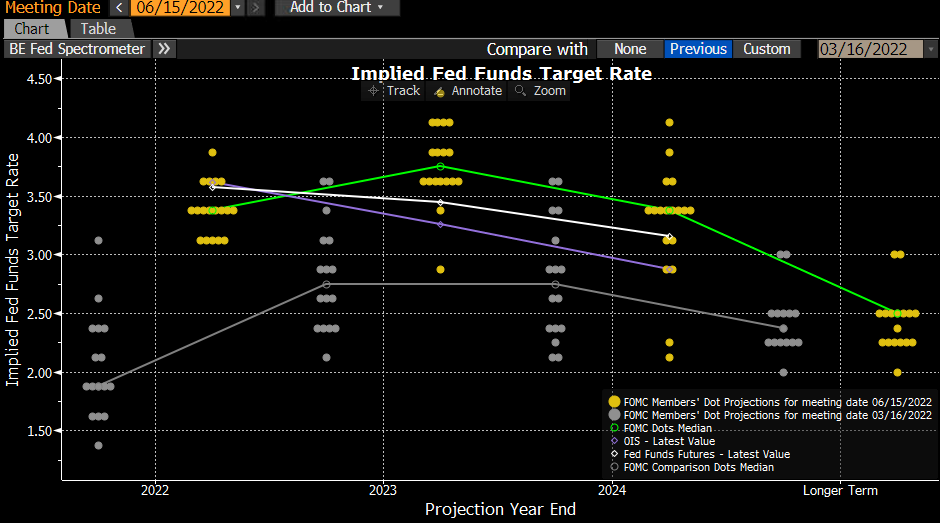

점도표 (Dot chart) 또한 두 가지 의미 있는 변화가 보였다. 첫째, 시장의 예상보다 더 높게 움직인 2022년 및 2023년 중간값을 통해 연준이 보다 앞당겨 금리 인상에 나서겠다는 확실한 신호를 보냈다. 둘째, 특히 2023년의 경우 3.75%의 중간값은 시장에서 반영하고 있던 수준보다 높은 수치로, 더 이상 뒤처지지 않겠다는 의지로 읽힌다. 하지만 여전히 2024년부터는 점진적으로 다시 금리 인하로 돌아갈 수 있음을 시사하는 모습.

3. 기자회견

런투노 귀에는 네 가지 주제에서 인상적인 발언이 나왔다.

3.1. 향후 정책금리 인상 사이즈 (75 bps or 100 bps?)

우선 서두 발언에서 파월 (Powell) 의장은 75 bps 인상은 이례적인 결정임을 강조하면서 시장의 기대치를 지나치게 높이지 않으려고 노력했다. 또한 다음 결정은 50 또는 75 bps라고 덧붙이면서, 최소 50 bps 인상을 고려하는 모습을 보임과 동시에 100 bps 인상에 대한 가능성은 차단하려는 듯한 인상을 줬다.

...Clearly, today’s 75 basis point increase is an unusually large one, and I do not expect moves of this size to be common. From the perspective of today, either a 50 or 75 basis point increase seems most likely at our next meeting. We will, however, make our decisions meeting by meeting, and we will continue to communicate our thinking as clearly as we can.

그리고 이어진 질의응답에서 FOMC를 앞두고 75 bps 인상 가능성을 언급한 Wall Street Journal 기자의 질문이 나왔다. 이에 대해서는 애매모호한 답이 나왔는데 기본적으로는 50 or 75 bps라는 위의 입장을 반복한 느낌.

NICK TIMIRAOS: So if you saw a movement like that again, another tick up in inflation expectations, would that put a 75 or even 100 basis point increase in play at your next meeting?

CHAIR POWELL: We're going to, I'll just say, we're going to react to the incoming data and appropriately, I think. So I wouldn't want to put a number on what that might be. The main thing is to get rates up and then pretty soon we'll be in an area where we're I think, as you get closer to the end of the year, you're in a range where you've got restrictive policy, which is appropriate, 40-year highs in inflation, we think the policy is going to need to be restrictive, and we don't know how restrictive. So, I think that's how we'll take it.

3.2. 기대 물가상승률 (inflation expectation)

기존 입장 (50 bps)에서 벗어나 75 bps 인상이라는 결정을 내린 배경을 설명하는 과정에서 지난주에 나온 미시간 기대물가지수 상승을 소비자 물가지수와 함께 중요한 이유로 언급.

CHAIR POWELL: So the preliminary Michigan reading, it's a preliminary reading, it might be revised, nonetheless it was quite eye catching and we noticed that. We also noticed that the Index of Common Inflation Expectations at the Board has moved up after being pretty flat for a long time, so we're watching that and we're thinking this is something we need to take seriously. And that is one of the factors as I mentioned. One of the factors in our deciding to move ahead with 75 basis points today was what we saw in inflation expectations. We're absolutely determined to keep them anchored at 2 percent. That was one of the reasons, the other was just the CPI rating.

3.3. 모델에 의존하지 않는 모습

점도표에서 제시했듯이 정책 금리가 3.8% 또는 4%에 도달하면 물가를 잡을 수 있는 것이냐는 질문에 대해 계량 모델의 예측 한계를 인정하고 보다 유연하게 대처하겠다고 답변.

CHAIR POWELL: I think it's certainly in the range of plausible numbers. I think we'll know when we get there really, I mean honestly though, that would be, you would have positive real rates I think and inflation coming down by then, I think you'd have positive real rates across the curve, I think that the neutral rate is pretty low these days. So, I would think it would, but you know what, we're going to find that out empirically, we're not going to be completely model driven about this, we're going to be looking at this, keeping our eyes open and reacting to incoming data both on financial conditions and on what's happening in the economy.

3.4. 근원 물가 상승률에 얽매이지 않는 모습 (에너지 및 식품 가격 상승도 중시)

공급 충격이 줄어들면 물가가 잡힐 것 같냐는 질문에 대해 의외로 근원 물가가 아닌 에너지 가격 및 식품 가격 (headline inflation)이 소비자들의 기대 인플레이션에 미치는 악영향을 언급하면서 공급 충격으로 인한 인플레이션이라고 해서 그냥 손 놓고 있지는 않겠다는 의지가 읽힘.

CHAIR POWELL. Well yeah, I think you've seen, again, we've been expecting progress and we didn't get that, we got sort of the opposite, so I also think the situation, really since the consequences of the Ukraine war become more and more clear, what you're seeing is the situation getting more difficult and you look around the world and I mean lots of countries are, lots of countries are looking at inflation of 10 percent and it's largely due to commodities prices. But all over the world you're seeing these affects. And so, and we're seeing them here. Gas prices are, all-time highs and things like that, that's not something we can do something about. So, that is really, and by the way, headline inflation, headline inflation is important for expectations. People, the public's expectations, why would they be distinguishing between core inflation and headline inflation. Core inflation is something we think about because it is a better predictor of future inflation. But headline inflation is what people experience, they don't know what core is. Why would they? They have no reason to. So that's expectations are very much at risk due to high headline inflation. So it's become, the environment has become more difficult, clearly, in the last four or five months and hence the need for the policy actions that we took today. Hence our resolution to get rates up and ultimately get them to where we think they need to be in coming months.

전반적으로 인플레이션을 반드시 잡아야 한다는 절박감이 여기저기서 확실히 드러났다.

4. 시장 반응

75 bps 인상은 거의 선반영하고 있었기에 오히려 시장은 발표 직후 금리가 내려갔다가, 상대적으로 매파적인 점도표로 인해 다시 금리는 상승. 그 후 기자회견에서는 buy the fact 흐름으로 금리 하락 시세. 아무래도 short cover 및 이벤트 이후 매수 물량이 더 컸을 것이라고 짐작한다.

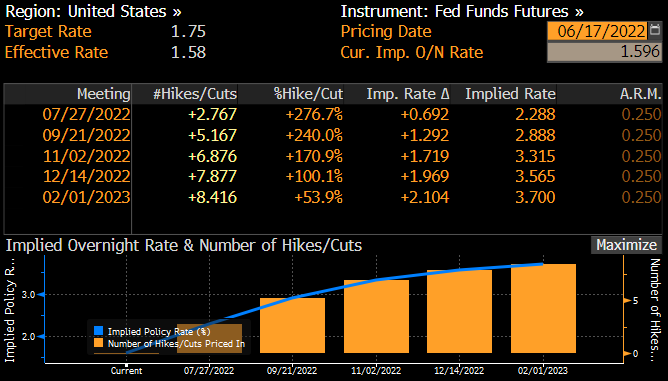

향후 정책 금리 경로 또한 이제 7월 FOMC도 75 bps 인상을 80% 정도 반영하고 있는 모습.

5. 향후 전망

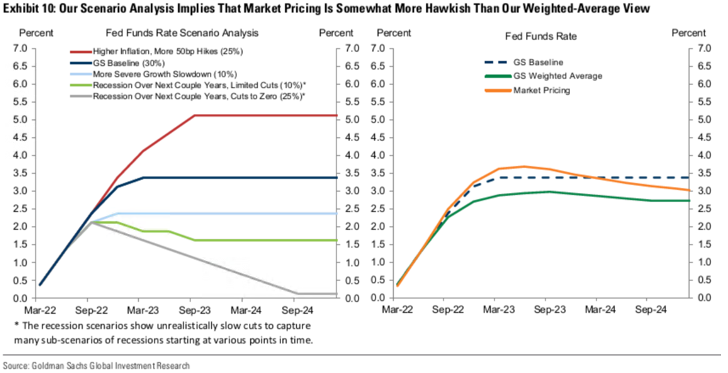

우선 연준의 향후 금리 정책 경로에 대해서 런투노는 여전히 현재 시장이 반영하고 있는 3% 후반 수준의 최종 금리는 45% 확률의 dovish case이고, 아래 그림의 왼쪽 붉은색 경로의 매파적 경로가 55% 확률의 base case로 판단한다. 8.5% 대의 소비자 물가지수 (CPI)가 4% 수준의 정책 금리로 쉽게 잡히지 않을 가능성이 더 현실적이라고 생각한다. 정책금리가 실물 경제에 영향을 미치는 데에 걸리는 시차가 존재하기 때문에 정책금리가 3% 중반에 도달하는 내년 초에도 소비자 물가가 6% 대에 머무는 상황이 올 가능성이 아직 더 높다고 예상하고 있다. 따라서 장기적으로는 여전히 금리의 상방압력이 더 높다고 본다.

하지만 단기적으로는 이제 연준을 비롯한 대부분 선진국 중앙은행들의 정책 발표가 지나갔기에, 당분간은 low volatility, risk parity rally 느낌으로 주식 및 채권 모두 6월 말까지 어느 정도 bear market rally를 이어갈 수 있는 국면이라고 판단하고 있다.

이 글이 마음에 드셨나요?

런던투자노트는 런던에서 일하는 현직 채권 트레이더의 금융시장, 투자 및 유럽 관련 블로그입니다.

런투노의 새 글들을 이메일로 구독하고 싶으시다면 아래의 링크를 눌러주세요.

'런던투자노트' 이메일로 구독하기

다음 링크를 통해 텔레그램 (Telegram)으로도 구독 가능합니다.

'런던투자노트' 텔레그램 채널 구독하기

'기관투자노트 > 중앙은행 정책' 카테고리의 다른 글

| 2022.7.21 ECB GC 복기 및 EUR 시장 전망: 50 bps hike & TPI into stagflation amid Italian (0) | 2022.07.22 |

|---|---|

| 2022.7.21 유럽중앙은행 통화정책회의 (ECB GC) 전망 (0) | 2022.07.19 |

| 2022.6.15 미 연준 FOMC 통화정책발표 전망: Why not hike 75 bps now? (3) | 2022.06.14 |

| 2022.6.9 유럽중앙은행 통화정책 (ECB GC) 발표 복기 (0) | 2022.06.12 |

| 2022.6.9 유럽중앙은행 (ECB) 통화정책회의 전망 (3) | 2022.06.09 |